Lodging Update: Providence, Rhode Island

By Rachel Roginski and Matthew Arrants

By Rachel Roginski and Matthew Arrants

Each quarter, Pinnacle Advisory Group prepares an analysis of the New England lodging industry, which provides a regional summary and then focuses in depth on a particular market. These reviews look at recent and proposed supply changes, factors affecting demand and growth rates, and the effects of interactions between such supply and demand trends. In third issue, we spotlight the lodging market in Providence, Rhode Island.

New England Summary

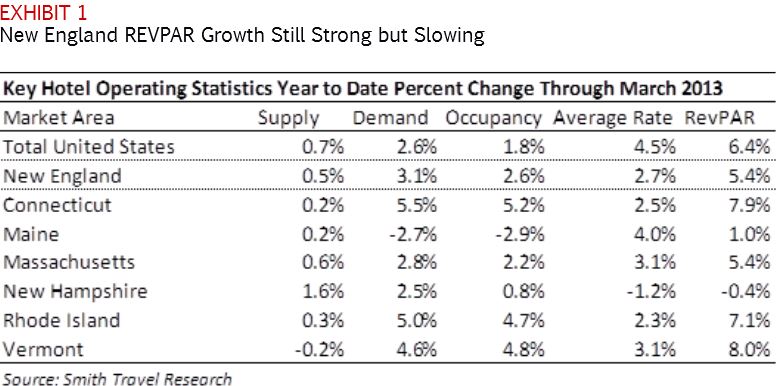

Revenue per available room (REVPAR) for the region grew by 5.4% in the first quarter compared to a growth rate of 5.6% for the year in 2012. While growth in the region lags behind the country as a whole, which had REVPAR growth of 6.4%, it is important to note that the first quarter is the slowest for the region due to seasonality and is the last to recover following economic downturns. The first quarter this year was also impacted by the extremely mild winter of 2012 and the fact that there were several weekend snow storms that impacted leisure travel.

Performance by State

Connecticut

Connecticut had a very strong first quarter, out-pacing the region and the nation as a whole in terms of REVPAR growth. The primary factors fueling the growth were limited new supply (0.2%) coupled with strong growth in demand, which together resulted in strong occupancy growth. Demand in Connecticut appears to be picking up steam, growing by 5.5% in the first quarter as compared to a decline of 0.3% for 2012. In Southwestern Connecticut, demand was fueled by a project at the submarine base in Groton that is expected to go through June. Demand in the Hartford area benefited from strong transient corporate travel.

Maine

Demand in Maine declined by 2.7% in the first quarter. That decline, coupled with a slight increase in supply, helped to push occupancy down from 41% to 39% for the state. This is surprising given the strong winter for skiing, but it reflects the fact that ski-related lodging represents only a small portion of total lodging supply in the state, and weekend snowstorms impacted non-ski travel. The state did, however, benefit from strong growth in average rate, which outpaced the rest of the region and the country as a whole, growing by 4.0% compared to only 2.3% for the year in 2012.

Massachusetts

Massachusetts experienced growth in demand of 2.8% compared to only 1.8% during 2012. Growth in supply remained fairly steady, at a manageable rate of 0.6%. Occupancy grew by 2.2%, which was above 2012 levels, but average rate growth slowed from 6.7% in 2012 to 3.1% during the first quarter of 2013. Occupancy levels are at their lowest levels in the first quarter (55% in the first quarter of 2013) as compared to the year as whole (66% for 2012). As a result, there is less of an imbalance between supply and demand and fewer high demand periods where operators can significantly drive their average rates. Therefore, average rate growth for the year is likely to exceed the 3.1% achieved in the first quarter.

New Hampshire

New Hampshire was the only state in the region to experience a decline in REVPAR during the first quarter. The decline is not surprising, given that it benefitted from the presidential primary elections in the first quarter of 2012. In addition, New Hampshire also had the strongest increase in supply, growing by 1.6%. The state’s occupancy performance would likely have been worse had it not been for strong demand from skiers and snowmobilers. The impact of the primary election demand in 2012 is most apparent in the decline in average rate. The primaries create a period of very strong demand that allows operators to increase rates significantly above what they normally charge during that time of the year, as election teams and members of the media flood the state.

Rhode Island

Demand for hotel rooms in Rhode Island grew by 5.0% in the first quarter, putting it just behind Connecticut in terms of growth in the region and well above the national average of 2.6%. It also represents a significant increase over its 2012 growth of 1.8%. This suggests that Providence, the largest market in the state, may finally be recovering from several years of lackluster performance. Average rate growth for the state, while above last year at 2.3%, was rather tepid as compared to the national average of 4.5%.

Vermont

The Vermont lodging industry continues to be very strong, with REVPAR growth of 8.0%. It was the strongest growth rate in the region, and follows on 2012 when it also finished with the strongest rate of growth at 7.7%. In addition to a very strong winter for skiing, the state also likely benefited from Canadian travelers encouraged by the exchange rate and by a decline in supply.

Anticipated Changes

We are watching several market areas over the next 6 to 12 months. These include the following.

Burlington, Vermont

The Hotel Vermont is expected to open in May with 125 rooms and 3,000 square feet of function space in a prime downtown location. A new Hilton Garden Inn is also under development with an expected opening in 2014. In suburban Burlington, a developer has plans to build a new Hampton Inn in Williston.

Cape Cod, Massachusetts

Hotel operators on the Cape are enthusiastic about the coming season, but many are concerned about the impact of the new train service between Boston and Hyannis. They are also concerned about the impact of the new Doubletree Hotel, which reopened at the end of July 2012 after being closed for 8 months and converting from a Radisson.

The Pioneer Valley, Massachusetts

In downtown Greenfield, a developer has proposed a 62-room Best Western through the adaptive reuse of a former department store. To the south in Northampton, there is speculation about the conversion of a former hospital to hotel use, and a local developer also has plans to build a new Fairfield Inn.

Portland, Maine

A large annual citywide convention that normally occurs in late May or early June has been pushed out of town this year, due to renovations at the Civic Center. Operators remain optimistic, as group booking pace looks strong and the Westin renovation is behind schedule, with the reopening date pushed back from Fall 2013 to Spring 2014.

Projections

The regional lodging market remains strong. Snow storms and colder weather, which had a negative impact on leisure travel though most of the region, were off-set by strong commercial demand.

With the strong demand, operators were able to increase average rates, leading to respectable growth in REVPAR. The continued growth in REVPAR has led to renewed development, with plans for new hotels throughout the region. While new supply is likely to impact some markets, meaningful new supply is not expected to impact performance until the middle of 2014 at the earliest.

Spotlight on Providence, Rhode Island

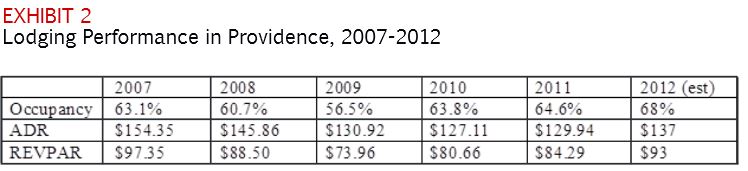

Providence is the capital of Rhode Island and the most populous city in the state, and it was one of the first cities established in the United States. Currently, there are nine hotels in Providence with a combined total of 2,295 guest rooms. The Providence lodging market has experienced cyclical occupancy and room rate patterns similar to regional lodging trends. However, while market occupancy has improved dramatically since the 2009 recession, room rates are still well-below levels before the recession.

Between 2000 and 2004, Providence’s market occupancy ranged from 70% to 77%. In 2005, market occupancy started to decline, hitting a low of 57% in 2009. Since that time, the Providence market has experienced substantial improvements, increasing to 64% in 2010, 65% in 2011, and 68% in 2012.

Although lodging demand has recovered, the average room rates in Providence have not. While ADR is improving with positive growth in 2011 and 2012, the steep decline between 2008 and 2009 will take years to get back to historic levels. Specifically, the ADR in 2007 was $154.35, but in 2009 ADR fell to $130.92 and then fell again in 2010 to $127.11. As a result of the stronger uptick in demand, and the recent ADR growth, the REVPAR in Providence reached $93 in 2012, but as noted in the table below, this falls well short of the $97 RevPar in 2007.The primary drivers of lodging demand in Providence are corporate, tourism, education, and groups attending meetings at conferences at the Rhode Island Convention Center. The education and healthcare sector is one of the largest employers in the metropolitan statistical area (MSA), anchored by the Lifespan Health System and Brown University. This sector accounts for 21% of total employment. In late 2011, state and city officials began developing a ‘Knowledge District’ in downtown Providence. Brown University spent $45.0 million to renovate a building for its medical school in this district. In addition, Johnson & Wales University plans to expand its campus, and the University of Rhode Island and Rhode Island College plan to build a joint nursing school for a reported $60.0 million in the Knowledge District. Headquartered in the City of Providence, RBS Citizens Financial

Group is one of the 15 largest commercial banking companies in the country, with a reported asset base of $140.0 billion. In the aftermath of the recent recession, the Providence region has started a long, measured process towards a recovery. Due to the weak business environment and the relatively high unemployment rate, revitalization in the Providence MSA will continue to progress, but at a slower rate than the nation as a whole.

Supply

There are no major changes planned with respect to new supply in Providence in 2013 or 2014. The most recent new supply increase was in 2009, when the Hampton Inn and Suites opened in downtown Providence. There have been several recent shifts in ownership and brand changes.

The Biltmore

The Biltmore was purchased in May 2012 from state receivership by Finard Coventry Hotel Management. The new owners acquired the hotel for $16 million and are in the process of conducting a $16 million, two-year renovation of the hotel. Once completed in early 2014, the hotel will operate as a three-diamond hotel, being positioned as “the finest, yet affordable hotel in the state”. The owners of the hotel recently agreed to a new collective bargaining agreement with the applicable labor union.

The Renaissance

The Renaissance was purchased by The Procaccianti Group and Rockbridge in early 2013 from Sage Hotels. Although it is not entirely certain, the hotel will likely remain a Renaissance by Marriott Hotel.

The Westin

In January 2013, the Westin Hotel was sold to Omni Hotels and immediately converted to the Omni brand.

The Sportsman Inn

The Sportsman Inn, a former adult entertainment venue, was purchased. It is rumored to be the subject of renovation and conversion to a 60–room boutique hotel. This hotel will probably not be open until late 2014 or early 2015.

Demand

Market segmentation for the Providence lodging market is approximately 70% transient and 30% group. The following is an overview of demand in each segment.

Transient

Approximately 70% of lodging demand in Providence is transient demand. This is comprised of both leisure transient and corporate transient types. Corporate transient demand is generated from visitors to local businesses, while leisure demand is primarily a function of tourism, as well the abundance of higher education in the city.

Commercial demand in Providence is generated primarily by the number of corporate tenants in the surrounding area. The downtown Providence office market ended 2012 with a vacancy rate of 16%, slightly higher than the 15.9% level at the end of 2011. There was significant positive absorption in the Class A sector, leading to the lowest Class A vacancy rate in nearly a decade. The largest generators of commercial room night demand include GTECH, AMGEN, RBS Citizens Financial Group, Hasbro, State of Rhode Island, City of Providence, Textron, Bank of America, CVS/Pathmark, Blue Cross Blue Shield, and the universities and hospitals.

Providence’s historical significance drives much of its tourism industry and produces significant leisure demand. The primary tourist destinations are along the Providence River and within downtown Providence. These attractions include the Providence River Walk, Roger Williams Zoo, John Brown House Museum, Battleship Cove, Providence Children’s Museum, Providence Piers, WaterFire Providence, Rhode Island School of Design Museum, Museum of Works and Culture, and various shopping districts including Federal Hill and the Providence Place Mall.

Within a half-hour drive of Providence is the Rhode Island coast and the very popular tourist destination of Newport. Most of the coastal Rhode Island communities have excellent access to the Atlantic Ocean, Narragansett Bay, and ancillary beaches.

In addition to tourism, there are several major colleges which provide significant leisure demand. These include Brown University, Rhode Island School of Design, Johnson and Wales, and Providence College. Leisure traveler demand is strongest on weekends in the spring, summer, and fall months.

Demand growth in the transient segment has been improving since the 2009 recession. While there are no major events, attractions, or developments underway that will dramatically increase transient lodging demand in the near future, overall economic improvement in Providence and the region will continue to spur modest growth.

Group

Meeting and group demand includes groups that reserve blocks of rooms for meetings, seminars, trade association shows, and other similar group gatherings. Meeting and group demand is typically strongest during the spring and fall months, while the summer months represent the slowest period for this market. Meeting and group travelers typically achieve an average length of stay of three-to-five days.

Meeting and group demand in the Providence area is driven by venues facilities in local hotels, university halls, the Rhode Island Convention Center, and the Dunkin Donuts Center. Providence’s five full-service properties (Biltmore, Hilton, Marriott, Renaissance, and Westin) are the primary hotels supporting group demand. These properties have combined meeting space of approximately 69,000 square feet.

The Rhode Island Convention Center, built in 1994, is the largest convention center in the State. This facility has approximately 100,000 square feet of exhibition space, 20,000 square feet of ballroom space, 23 meeting rooms, and 30,000 square feet of pre-function space. It is connected to the Dunkin Donuts Center. The Rhode Island Convention Center had an excellent year in 2012. According to the

Tap Report, there were 153 definite events in 2011, compared to an estimated 178 events in 2012. Total room night demand from the Convention Center in 2011 was 287,602, while room night demand from the Convention Center was an estimated to have increased 11% increase in 2012.

The strength of the Convention Center was one major factor in the continued upturn in demand in the Providence lodging market. Based on both the definite and tentative booking at the Convention Center, 2013 should be a reasonably good year for group demand in Providence.

Demand Conclusion

Lodging demand in the Providence market is expected to continue to experience modest growth into the foreseeable future. Corporate, leisure and group demand growth is expected to experience gradual, measured growth in the absence of any major corporate expansions, new attractions, or more robust group and convention demand in the market. In 2012, overall lodging demand growth in the Providence was approximately 4%. We expect positive, albeit slower, growth in 2013 in all demand segments within the lodging markets.

Average Rate

Room rates are the biggest challenge within the Providence market. While average daily rate (ADR) increased above 5% in 2012, average room rates are still well below historic room rate levels. At its peak in 2007, the ADR in Providence was $154. After several years of declining room rates, the mark reached bottom with $127 in 2010. In 2011, the ADR improved slightly to approximately $130. Most recently, the ADR reached $137. And while the local operators are pleased with the uptick in room rates, the Providence market still has a way to go until it reaches the peak ADR.

2013 looks promising for ADR growth. Changes in ownership, re-branding, and renovations will likely mean higher rates, as owners push the operators to gain above inflationary room rate increases.

Room rates are up over 3% year-to-date in Providence, and by year-end we expect to see room rates increases of 4%

Projections

We expect 2013 to be an improvement over 2012 for the Providence lodging market. Specifically, we expect occupancy to grow by approximately 1%, with average rates growing by 4% for a REVPAR increase of approximately 6%. There is no new supply for 2013, and the substantial renovation at the Biltmore, along with various flag changes and ownership, all bode well for the Providence lodging market. Furthermore, without new supply in 2014, the Providence lodging market should once again see an upward trend in occupancy, room rate, and REVPAR.

Rachel J. Roginsky, ISHC, is the owner of Pinnacle Advisory Group. She has more than 30 years of experience in hospitality consulting. Ms. Roginsky is a board member of numerous organizations related to hospitality, is a regular guest lecturer at the Cornell Hotel School, and is co-editor of five leading hotel investment books. Email rroginsky@pinnacle-advisory.com