What Role for the Resilience and Sustainability Trust in Creating Fiscal Space for Climate Vulnerable Countries?

By Jwala Rambarran and Sara Jane Ahmed

The Fourth International Conference on Financing for Development (FfD4), which takes place at the end of June in Spain, will attempt to forge the main global policy framework for development finance over the next decade and presents a critical opportunity to tackle systemic inequities in the global financial system.

As the international community approaches this pivotal moment, climate vulnerable countries in the Global South find themselves grappling with a worsening debt crisis that both threatens their development prospects and deepens their climate vulnerability, demanding urgent action.

A new technical paper from the Task Force on Climate, Development and the International Monetary Fund explores how the International Monetary Fund (IMF)’s latest lending instrument – the Resilience and Sustainability Trust (RST) – can play a greater role in the broader reform of the global debt and financial architecture. The policy brief draws upon the initial RST experiences of two climate-vulnerable Caribbean countries – Barbados and Jamaica.

Looming Global South debt crisis

Debt distress now threatens more than half of the 68 low-income countries eligible for the IMF’s Poverty Reduction and Growth Trust—more than double the figure in 2015. Moreover, the latest World Bank’s International Debt Report highlights a worsening debt crisis among low-income nations, with interest payments soaring in 2023 to four times higher than a decade ago. Even nations with access to international capital markets, such as Argentina, Ecuador, Suriname and Sri Lanka, are experiencing debt distress.

While debt can serve as a powerful tool for economic growth and development, prioritizing debt repayments at the expense of essential public services and investments can have devastating consequences. In 2023, a historic 54 developing nations allocated more than 10 percent of their government budgets to servicing debt interest payments. As these governments struggle to meet their obligations, citizens bear the heavy cost: schools remain underfunded, hospitals face chronic shortages and critical infrastructure deteriorates. Today, over 3.3 billion people live in countries where debt interest payments exceed spending on health or education.

Private creditors have extracted more in debt service than they have provided in new financing, deepening financial strain. This is not merely a liquidity challenge but also a solvency crisis. Despite these challenges, existing global debt relief mechanisms, including the Group of 20 (G20)’s Common Framework, remain inefficient, costly and in dire need of reform. As a result, many governments go to great lengths to avoid defaulting on their debts—even if it means sacrificing their development goals. Without urgent reforms, this growing debt crisis will only worsen, stifling economic growth, exacerbating inequality and leaving millions of people vulnerable to the impacts of climate change

Climate change and debt

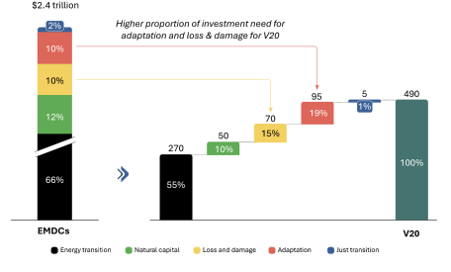

While addressing the mounting debt crisis is urgent, developing countries are also grappling with the even more pressing threat of climate change. The Independent High-Level Expert Group estimates that Global South countries (excluding China) will need $2.4 trillion of climate finance per year by 2030, of which around $1 trillion per year is external finance, to accelerate the transition to low-carbon economies in line with the Paris Agreement. The Vulnerable 20 (V20) Group, a group of 70 countries highly vulnerable to the climate crisis, need an estimated $490 billion per year in climate finance, with a higher proportion of investment needed for adaptation and to address loss and damage.

Figure 1: Estimated annual climate finance for Global South countries (excluding China) and the V20 by 2030, USD billion

These considerable amounts are well beyond the limited fiscal space of many developing countries, especially those with rising debt burdens. This dual debt-climate challenge requires coordinated solutions that integrate debt relief and climate finance, paving the way for sustainable, resilient growth.

As the primary multilateral, rules-based institution responsible for promoting global macroeconomic and financial stability, the IMF has a central role to play in helping its member countries urgently unlock and mobilize substantial, affordable climate finance while supporting reforms to the international debt architecture.

The RST and establishing a link between debt and climate finance

The IMF should be commended for establishing the RST in April 2022. Through the RST’s lending arm, the Resilience and Sustainability Facility (RSF), the IMF provides concessional, longer-term financing to help eligible member countries address macro-critical structural challenges, including climate change.

By early March 2023, the IMF’s Executive Board had swiftly approved RSF arrangements for five pilot countries—Costa Rica, Barbados, Rwanda, Bangladesh and Jamaica—alongside concurrent IMF-supported programs. By the end of December 2024, the number of RSF programs had expanded to 21.

Looking ahead, a key question remains: How can the IMF ensure that the RST addresses a major gap in the global debt and financial architecture—namely, providing balance of payments support for countries facing prospective climate shocks and green transitions to foster resilient and sustainable growth over the medium term?

An initial assessment of the RSF experiences in two Caribbean pilot countries—Barbados and Jamaica—offers valuable insights for shaping future RSF-supported programs. One key recommendation relates to the IMF leveraging RST resources to establish a link between debt and climate finance.

By taking on more debt to combat climate change, Global South countries find themselves trapped in a vicious cycle of debt and climate vulnerability. When designing future RSF arrangements, particularly for these highly indebted, climate-vulnerable countries, the Task Force recommends that the IMF should consider deploying more RST resources to create fiscal space for climate action through debt relief solutions that are timely, fair and effective. This could involve linking debt relief options—such as debt pause clauses, debt restructuring, reprofiling and debt swaps—to investments in green resilience policies aligned with national climate and development plans.

Barbados’ recent debt-for-climate resilience swap serves as a strong illustrative case of how debt relief can empower countries to prioritize climate resilience. By buying back $165 million of high-cost debt, Barbados redirected these resources to invest in essential infrastructure like water systems, food security and environmental protection—ultimately strengthening the country’s capacity to withstand climate shocks.

While debt relief is essential for Global South countries to meet their climate and sustainable development goals, it is not a silver bullet. Broader reforms to the global financial architecture are necessary. At the heart of calls to reform the global debt system is the demand for a UN Framework Convention on Sovereign Debt. This framework would include agreements on a multilateral sovereign debt resolution mechanism, binding responsible lending and borrowing principles, an automatic suspension of debt payments in the event of catastrophic external shocks, and new approaches to the IMF’s debt sustainability frameworks.

Additionally, the Task Force continues to advocate for the IMF to issue new Special Drawing Rights (SDRs) and rechanneling unused SDRs through multilateral development banks (MDBs) to reinforce regional liquidity and ensure these concessional resources are used to maximum effect.

Conclusion

As the FfD4 approaches, there is even greater need for the global community to unite around bold, concrete actions to overhaul the international debt system. Moreover, the IMF must continue to expand its toolkit—linking debt relief to climate action, building the case for concessional capital, creating fiscal space and incentivizing green resilience policies. These are important steps that FfD4 and the IMF can take toward a healthier global economy, a liveable planet, common prosperity and trust-building so crucial in today’s increasingly polarized geopolitical landscape.

Read the Technical Paper*

Never miss an update: Subscribe to the Task Force on Climate, Development and IMF newsletter.