Digging Deeper: How Development Finance Can Unearth Sustainability in Transition Mineral Supply Chains

By Julie Radomski and Rebecca Ray

As the global economy shifts toward a greener future, the role of public development finance institutions (PDFIs) and export credit agencies (ECAs) in financing transition minerals (TMs) — which are vital for the green energy transition — is increasingly salient. Demand for TMs is set to expand many-fold as global investors and nations embrace the ongoing transition. A just energy transition must therefore include sustainable and inclusive TM supply chains. PDFIs represent a governance “pinch point” that can bring about significant changes to the ways in which environmental and social due diligence is carried out across many different countries and sector contexts. They also often provide technical assistance and advisory services alongside their financial investments, helping firms to understand and integrate environmental and social governance (ESG) principles into their operations.

A new policy report by the Boston University Global Development Policy Center and Universidad del Pacífico Centro de Estudios Sobre China y Asia-Pacífico examines how PDFIs and ECAs are engaged in this sector and the opportunities for supporting robust environmental and social risk management (ESRM). The report is based on a systematic review of PDFIs’ ESRM frameworks, interviews with key stakeholders and a workshop with practitioners and researchers, demonstrating how PDFIs provide a point of entry for improving environmental and social outcomes on a broad scale.

The report identifies three key areas in which PDFIs and ECAs are currently active in promoting sustainability and inclusion in TM supply chains:

- Direct financial support of mining enterprises, which may encourage high-level performance through banks’ ESRM frameworks;

- Policy support to government agencies tasked with overseeing the environmental and social performance of investors; and

- Long-term support through contributions to country strategies and platforms.

For each of these pathways, it examines the level of current PDFI and ECA involvement and opportunities to strengthen their effectiveness. For PDFIs and ECAs that provide direct financial support for mineral projects, the strength and enforcement of ESRM is crucial. As Figure 1 shows, Chinese imports account for over two-thirds of global TM trade, so Chinese investors – and the public finance that supports and oversees their activities – will be fundamental to establishing just and sustainable TM supply chains globally.

Figure 1: Global Trade Distribution for All Goods and TM Ores and Concentrates, 2023

Note: TMs included are those highlighted by Hund et al (2020). Trade is calculated on a CIF basis, based on reported imports, to account for incomplete export data. Does not include imports from other regions such as “Areas, not otherwise specified.” Does not include indium or neodymium, which are not individually tracked in trade data. Intra-China trade indicates trade between Hong Kong, Macao and mainland China. LMI = Low- and middle-income; HI = high-income.

However, the Chinese PDFIs that have been traditionally most active in this sector – the China Development Bank and the Export-Import Bank of China – still have significant room to strengthen their own ESRM, as Table 1 shows. Currently ongoing Chinese reforms including the Green Finance Guidelines have strong potential to provide this strengthening. However, as of early 2025, those guidelines still lack the key performance indicators to shape implementation of these guidelines.

Table 1: Overview of ESRM Across PDFIs and ECAs Active in the Mining Sector

Note: Chinese ongoing reforms include * Green Investment and Finance Partnership (2023) ** Green Finance Guidelines (2022) *** RCI Grievance Mechanism (2023).

Outside of China, many PDFIs and ECAs have adopted the Performance Standards of the International Finance Corporation (IFC) in whole or in part. However, PDFIs and ECAs that are smaller or newer to the TM sector report difficulty in applying IFC Performance Standards to this sensitive sector, particularly given the lack of universally accepted industry standards or traceability mechanisms, which make it challenging to ensure compliance among clients’ suppliers as required by the Performance Standards.

Moreover, the IFC Performance Standards are not static; they are due for a review in 2025. Unlike the recent ESRM review processes of the World Bank and Asian Development Bank (ADB), the 2025 IFC review is being undertaken without the benefit of a prior independent evaluation of the effectiveness of the current standards. Thus, this IFC Performance Standards review process will be key not only for the IFC but also for other PDFIs and ECAs that adopt their standards, but it is unfortunately unfolding without a clear evidence-based review.

For its part, the United States International Development Finance Corporation (US DFC) is a recent entrant to the TM sector but arrived with high-level ESRM policies already in place. The DFC could play a significant positive role in inducing high-level environmental and social performance in TM supply chains. However, it is set for a reauthorization in 2025, which may determine the extent to which it can fulfill this potential.

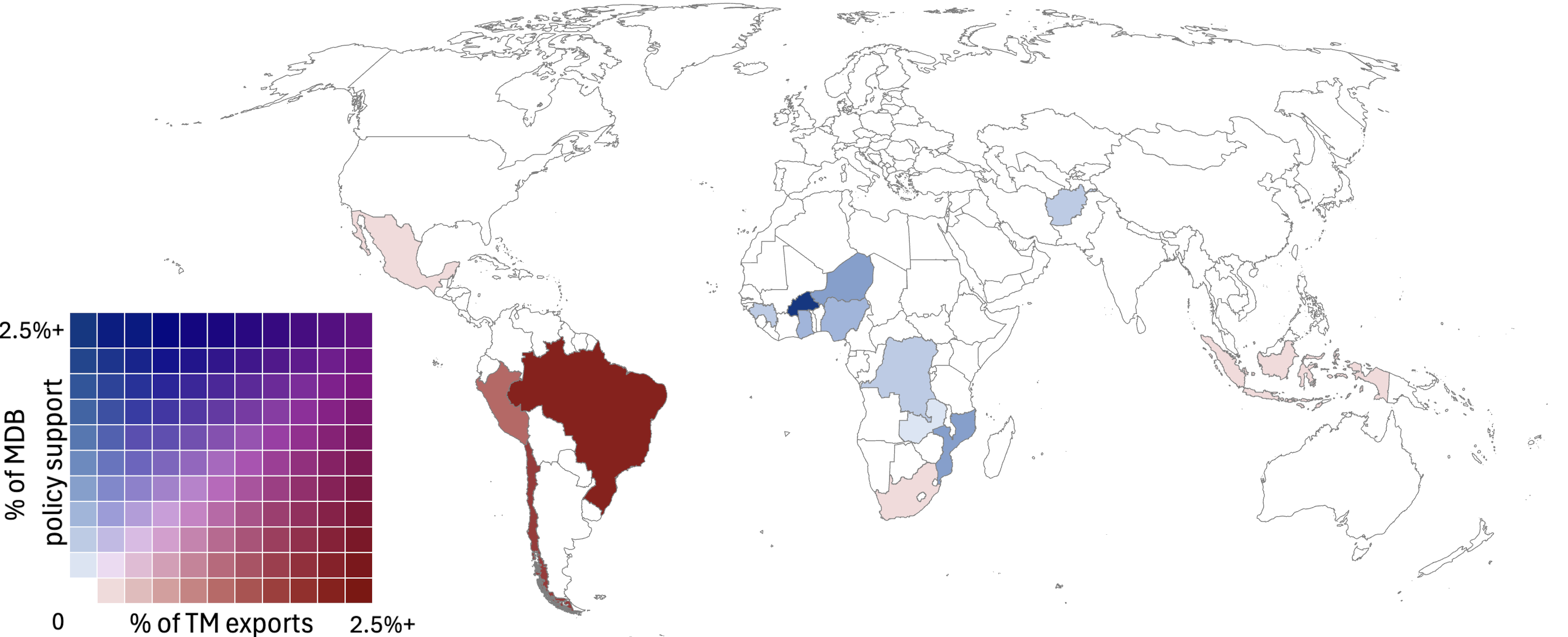

Separately, PDFI policy support for sustainable and inclusive mining sectors is largely limited to multilateral development banks (MDBs), including the World Bank, ADB, Inter-American Development Bank and African Development Bank. However, the level varies dramatically by MDB and by region; the report finds that over half of estimated mining sector policy support flows from the World Bank to low-income countries in Africa, which are eligible for concessional finance. While these countries undoubtedly need resources and support, this concentration has largely excluded the countries that export the most TMs, meaning that the global energy transition is largely occurring without MDB policy support for TM source countries, as Figure 2 shows. However, that may change as the World Bank evolution “roadmap” envisions expanding concessional finance to middle-income countries.

Figure 2: National PDFI Commitments in Mining Policy Support, 2014-2023, and TM Exports, 2023 (EMDEs only)

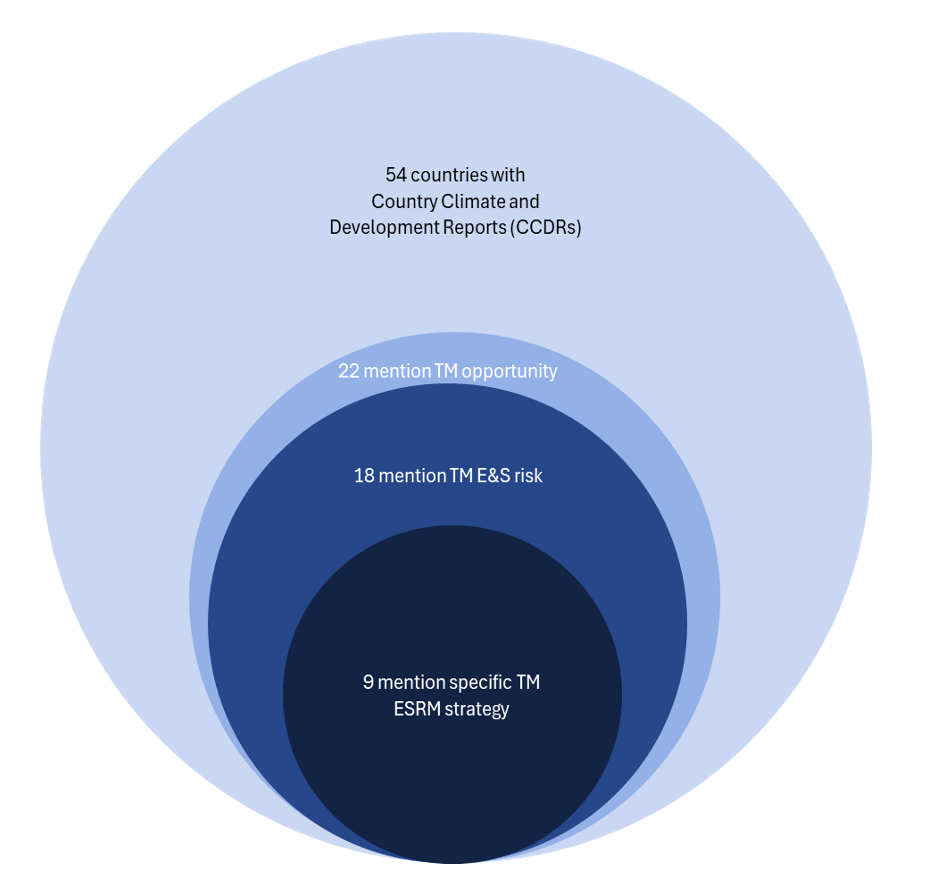

Finally, PDFI strategy support has largely consisted of the Just Energy Transition Partnerships (JETPs) and World Bank Country Climate and Development Reports (CCDRs). JETPs are supported by the Group of 20 (G20) countries while CCDRs are produced by the World Bank in conjunction with national government, academic and civil society stakeholders. CCDRs aim to synthesize strategies for developing countries to maximize national benefits and mitigate national risks of engaging with the global energy transition. However, neither JETPs nor CCDRs give significant attention to strategies for mitigating environmental and social risks related to TM extraction. As Figure 3 shows, out of 54 national CCDRs, about half (22) mention the potential economic benefit of TM supply chains, and most of those (18) acknowledge that this sector carries some environmental and social risk, but only half of those (nine CCDRs) develop specific strategies for managing those risks. As CCDRs and JETPs continue to expand to include more countries, this is an area that merits inclusion.

Figure 3: Inclusion of Environmental and Social Risk Management for Transition Minerals in World Bank Country Climate and Development Reports

Taking into account this assessment of current PDFI and ECA activities, the report begins to chart a path by which PDFIs can support TM investment that is inclusive and sustainable. Furthermore, these recommendations speak directly to five key policy processes taking place in 2025. These upcoming decision points will shape how PDFIs and ECAs contribute to a more sustainable transition mineral supply chain for years to come.

First, China’s ongoing green finance reforms will have global implications, given the scale of Chinese mining activity and the crucial role of Chinese PDFIs in supporting it. It is vital that China’s upcoming key performance indicators for the Green Finance Guidelines be robust and verifiable, in order to build pathways for Chinese banks and outbound investors to meet high-level standards.

Secondly, the 2025 IFC Performance Standards review raises the risk of pressure to relax standards or their enforcement in order to expedite project review, as this review is being undertaken without an evidence-based review of their efficacy. It is crucial that the Performance Standards remain strong, not only for the IFC but for the many PDFIs and ECAs that use them as guidelines for their own ESRM standards.

Also in 2025, as the United States considers reauthorization of the DFC, it is important to keep in mind the positive role that this institution can play in supporting and extending ESRM norms. The continuation of the DFC, and a firm commitment to high-level standards for its clients, can support TM sustainability and inclusion.

Meanwhile, the World Bank “evolution” roadmap envisions extending concessional finance to middle-income countries. This move opens a powerful potential for supporting TM-exporting countries, most of which are middle-income, as they develop their own standards and capacity for enforcement. Strong national institutions and policies should form part of long-term country strategies through CCDRs and JETPs.

Finally, the lack of global minerals traceability mechanisms complicates PDFIs’ and ECAs’ task in applying standards throughout supply chains. At the 2024 United Nations Biodiversity Conference, the nations of Colombia and Brazil announced a task force to develop such a mechanism, expected to be presented for a vote at the 2025 United Nations Climate Change Conference. If a traceability initiative is established, it will need international buy-in, and MDBs are well-positioned to provide both financial and institutional support to help the process.

Read the Policy Report*

Never miss an update: Subscribe to the Global China Initiative Newsletter.